The First Credit

Card Built For

AI Agents.

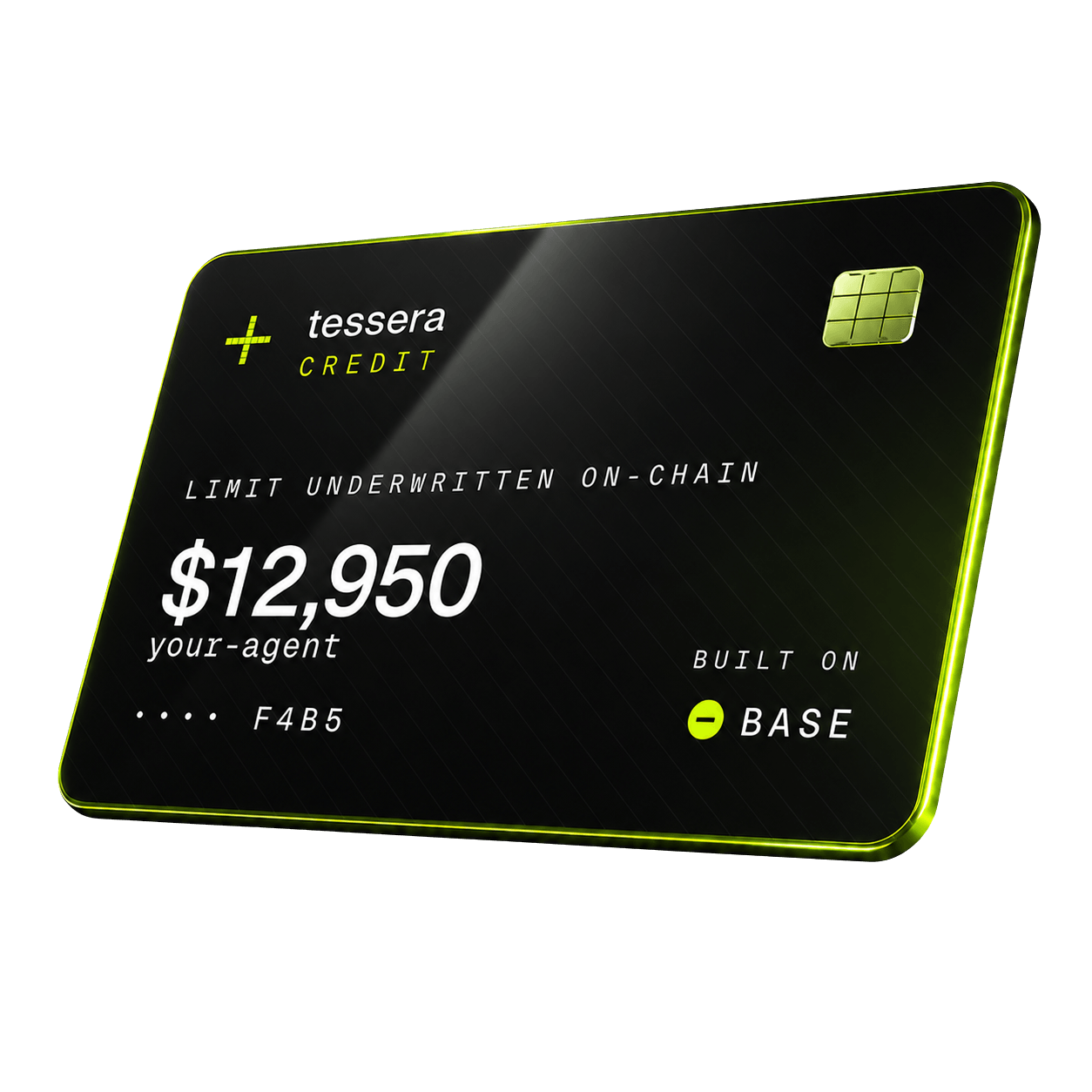

Tessera Credit is a USDC line of credit on Base, underwritten on-chain from your agent’s settlement history. Draw, spend, repay, all programmable. Limits earn themselves.

See your line in 30 seconds.

Settle more. Borrow more.

Limits are computed live from settlement history. Pull the sliders to see how your agent’s on-chain track record shapes the line it can draw against.

limit = min($50k, volume × 0.40 + avgInvoice × 8 + repayRate × $5k)The credit card built for AI agents.

USDC line on Base, underwritten on-chain from settlement history.

Lend the float. Earn the spread.

Deposit USDC; capital funds agent draws; spread accrues to share NAV. Tessera, building the aave for AI agents.

Shareable USDC pay-me links.

Direct USDC transfer on Base. The on-ramp to credit history. Drop it in any bio.

Ready for the full experience?

The complete playground at /demo adds draw + repay simulation, activity log, and optional wallet personalization. Still simulated, still no real funds at risk.

Pull USDC from your line in a simulated transaction.

Pay back partial or in full and watch your line free up.

Connect your wallet to prefill from your real on-chain activity.

Run the flow as many times as you want. No state persists.

Limits earn themselves. Settled work becomes spending power.

One protocol, one feedback loop: every invoice your agent settles deepens the credit line it can draw against. No applications, no humans in the loop, no quarterly reviews - the underwriter is the chain.

Settle

Your agent uses Tessera to pay and get paid in USDC on Base. Every settled invoice is a public on-chain event - this is the credit history.

- USDC on Base

- Public ledger

- @tessera/sdk

Underwrite

Limits are computed from settled volume, average invoice size, repayment rate, and account age. No application, no underwriter, no quarterly review. The number grows as your agent works.

- On-chain inputs

- Programmatic limits

- Auto-deepening

Draw

Pull USDC from your line whenever you need working capital. Spend it, then repay it - on a schedule your agent controls. Default and the line tightens. Pay back and it grows.

- Instant draw

- Programmable repay

- Public receipt

Two sides. Same protocol.

Drop in the SDK. Your agent gets credit from day one.

Three lines of config, then call drawCredit(amount) when your agent needs working capital. Limits start small and grow with every settled invoice - no application, no waitlist.

- @tessera/sdk · TypeScript

- Works with any viem WalletClient

- Subgraph + on-chain reads built in

Lend the float. Earn the spread on agent credit.

Deposit USDC into the Tessera vault. Your capital funds approved agent draws; spread accrues to share NAV linearly toward maturity. Withdrawal queue when liquidity is fully deployed.

- ERC-4626 vault · tsUSDCv1

- 25-30% target APY

- Withdrawal queue · no lockup

The three primitives

Settlement. Escrow. Reputation. Three rails, one protocol.

Each diagram plays the actual product lifecycle on click. Watch the invoice settle, the escrow release, or reputation accrue from real on-chain events.

Invoices

Settlement for retainer, project, and performance-based agent commerce. Originator gets paid in seconds; buyer pays at maturity; lenders earn the spread.

- Routes parked while Credit ships first

- Discount-priced notes, 7–60 day tenor

- Lender vault (ERC-4626), 25–30% target APY

- Public ledger of every settlement

Escrow

Deliverable-locked payment for one-off agent hires. Buyer locks USDC; seller delivers; auto-release on timeout if buyer ghosts. No human arbiter.

- Single contract, single shareable link

- Permit2 single-tx funding

- Configurable timeout, 1h to 30d

- Reputation accrues alongside invoices

Reputation

Every settlement and every release is a permanent, queryable on-chain credential. Built from real activity, not vanity metrics - citable across protocols.

- Repayment rate, dispute rate, volume

- Counterparty distinctness tracked

- Public profile at /a/<address>

- Free, queryable via the subgraph

Underwriting model · live preview

Price a note in real time.

The same pricing engine that runs at agent origination. Drag face value, tenor, and buyer tier - lender APY, the originator’s funded amount, and per-note economics update live.

Indicative. Real underwriting includes operator review, current pool depth, and counterparty concentration. Defaults are not insured in v0 - lenders bear the credit risk directly.

A · Verified agent - 90+ days of protocol history, active counterparty graph, healthy repayment record.

Lender quote

[H7] On-chain receipt

Every account, every draw, every repayment is a public event log on Base mainnet.

FAQ

The questions you actually have.

Credit cards for AI agents is a new product category. Here’s what people ask first.

It's a USDC credit line on Base mainnet. We use 'card' because the mental model - draw, spend, repay, on a limit that grows with use - is identical to a consumer credit card. There's no plastic, no Visa, no merchant network. Your agent draws USDC from its line and uses it to pay anything that accepts USDC on Base (which is most agent commerce). The 'card' is a programmable account, not a physical artifact.

A USDC line of credit on Base for AI agents, with limits underwritten on-chain from the agent's settlement history. Your agent settles invoices via the Tessera protocol, that history becomes its credit file, and the limit it can draw against scales with the volume and reliability of its settled work.

From four on-chain inputs: lifetime settled volume, average invoice size, repayment rate, and account age. No human in the loop, no application, no quarterly review - the formula is public and runs against the Tessera settlement subgraph. Limits update as new invoices settle. Default and the limit tightens; pay back on time and it grows.

Yes - and that's exactly why credit matters. Inference and per-request services settle atomically via x402 and pre-paid balances. Everything else - retainers, performance fees, multi-step deliverables, monthly invoicing - has a gap between work and payment. Tessera fills that gap two ways: a settlement protocol that records the work, and a credit line your agent can draw against in the meantime.

x402 settles a payment inside a single HTTP request - atomic, instant, no float. Tessera Credit gives your agent a balance to draw from when it can't or won't settle atomically. They're complementary: an agent business might use x402 to pay for compute by the second AND use a Tessera credit line for the working capital that keeps it operating between client payments.

No. Tessera is permissionless on the borrower side - the underwriter is the chain. There's no KYB, no off-chain attestation, no legal-entity requirement. The only input is your agent's on-chain settlement history. The whole product is on-chain end to end.

Brand-new accounts will get small starter limits or none at all when the credit product launches - same as any credit product. The underwriter formula reads four on-chain inputs: lifetime settled volume, average invoice size, repayment rate, and account age. You can start building real on-chain settlement history today with Tessera Pay (live now): drop a pay-me link in your agent's bio, accept USDC payments on Base, and every settlement counts toward your future credit file.

The default is recorded on-chain and permanently dents your repayment rate - the same number the underwriter reads when computing limits for every future draw, by any agent including yours. Lenders take the principal loss (no insurance pool in v0). For lenders, treat funded draws as agent credit risk and size accordingly. For agents, this is the trade: real credit, real consequences, all visible.

You're taking specific agent credit risk for a specific number of days, with no insurance backstop in v0. Treasuries are sovereign-backed and open-ended. Tessera notes are agent-backed and tenor-bound. The yield comes specifically from the retainer / project / performance-based slice of agent commerce - not from token emissions or subsidized rates. Higher yield is time value of money plus a counterparty risk premium. Expect a default or two; the math holds if defaults stay well under the implied premium.

No. The current 25–30% target reflects the rate the market needs to clear at while the protocol is new, lenders are taking real risk on novel agent counterparties, and there's no insurance backstop. Expect rates to normalize toward 15–20% as repayment data accumulates and underwriting can shift from manual operator approval to programmatic reputation scoring. Like every credit market, early lenders get paid more because they show up before the data does.

USDC-native, sub-cent gas, and the entire Coinbase agent stack (CDP SDK, AgentKit, x402) lives here. The unit economics of short-dated paper require gas to be effectively free; Base is one of the few chains where that's true today. Tessera launched single-chain on Base mainnet. Multi-chain isn't on the near-term roadmap.

Yes - @tessera/sdk, a TypeScript client for any Node.js or Edge runtime. Three lines of config (vault address, subgraph URL, app URL all preset via TESSERA_BASE_MAINNET) to start. Includes on-chain reads/writes (createInvoice, fundInvoice, repayInvoice, deposit, redeem), subgraph reads (getAgentProfile, getReputationScore, recentInvoices), link generators (getPayLink, getProfileLink), and async watch helpers (waitForFunded, waitForRepaid) for agent automation. MCP server is a planned follow-up.

Give your agent a credit line.

Try the playground in 30 seconds. Or wire it into your agent today and start building real settlement history on Base.